June 2026

Market Conditions Improve as Sales Rise and Available Inventory Declines

The Greater Toronto Area housing market showed a meaningful improvement in June 2026. Sales activity increased compared with the same month last year, fewer new properties entered the market, and the total number of active listings declined.

These changes indicate that demand strengthened while supply tightened. This represents a significant shift from the conditions experienced earlier in 2026, when cautious buyers and elevated inventory placed greater pressure on sellers.

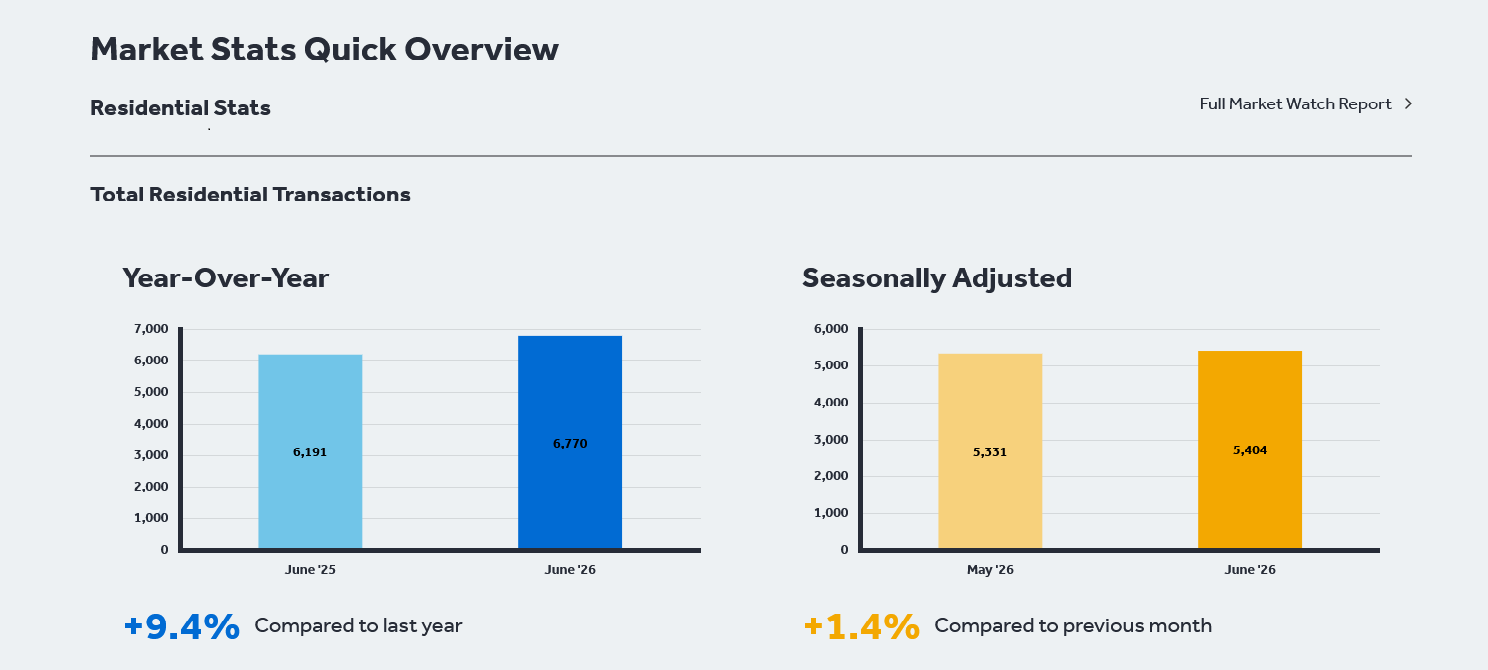

A total of 6,770 homes were sold through the TRREB MLS® System in June 2026. This was an increase of 9.4 per cent compared with the 6,191 sales recorded in June 2025.

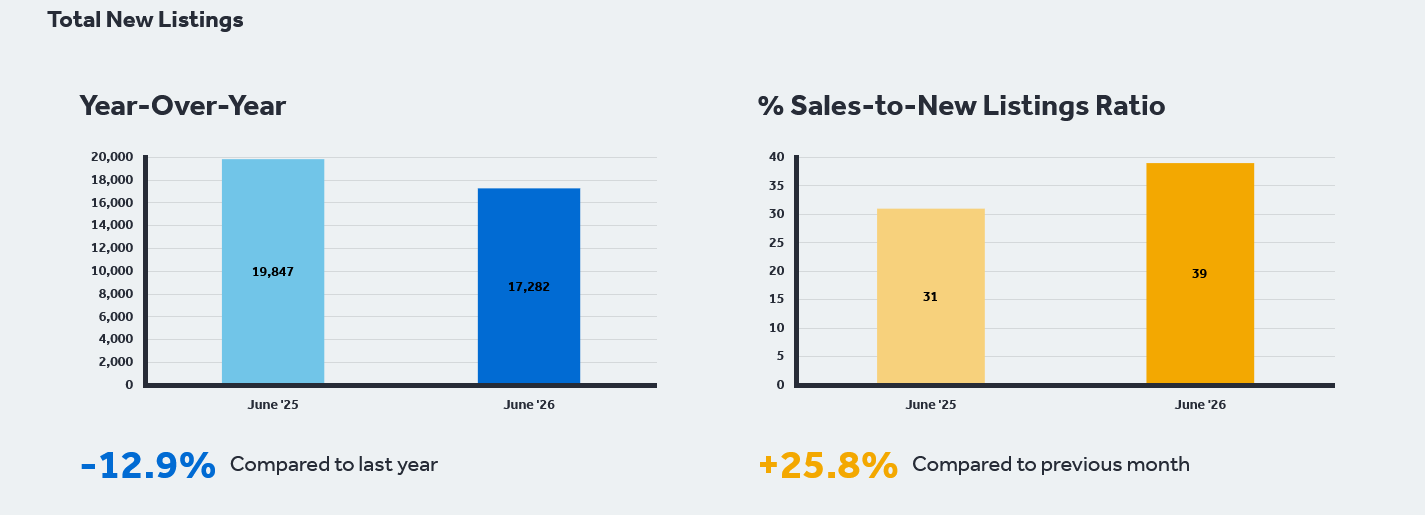

New listings moved in the opposite direction. A total of 17,282 new listings entered the market, down 12.9 per cent from 19,847 one year earlier. Active listings also declined, falling 13.5 per cent from 31,585 in June 2025 to 27,329 in June 2026.

The combination of rising sales and declining inventory is the most important development in the June report. It shows that buyers are returning to the market at the same time that the available supply of homes is being reduced.

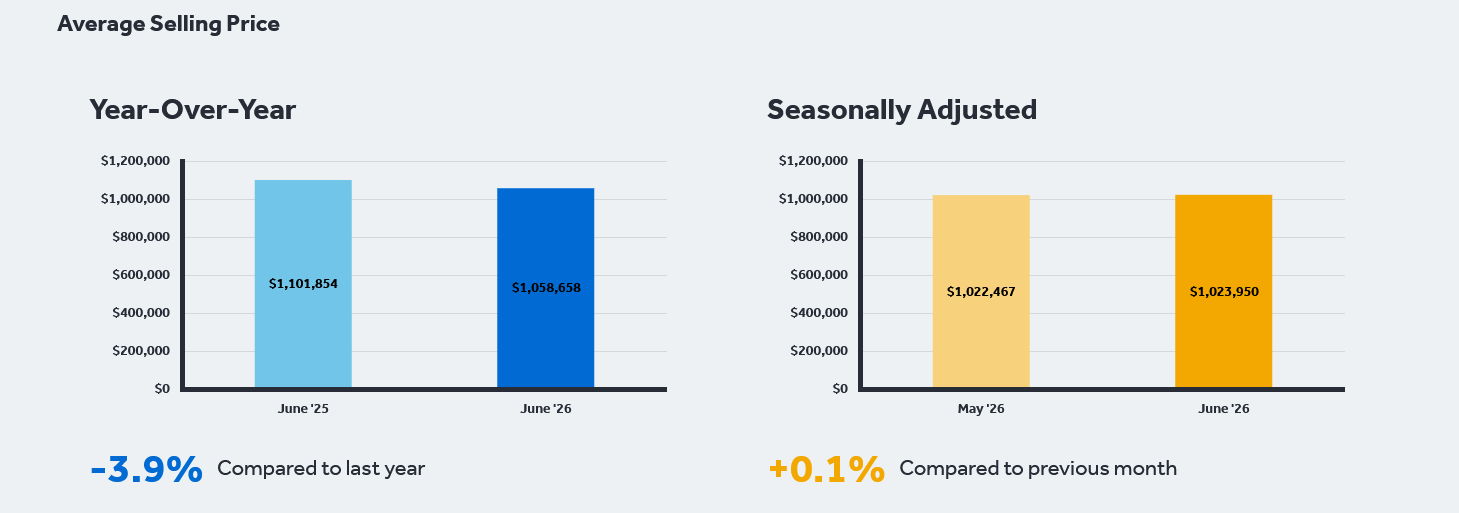

Prices remained below last year’s levels, however. The average GTA selling price was $1,058,658, down 3.9 per cent from $1,101,854 in June 2025. The MLS® Home Price Index Composite benchmark declined by approximately 5.4 per cent year over year.

The market is therefore not experiencing broad price growth yet. Instead, it appears to be moving from weaker conditions toward greater stability.

This distinction is important. Stronger sales do not automatically mean that every property will sell quickly or that sellers can increase their asking prices without supporting evidence. Buyers remain informed, selective, and sensitive to affordability. At the same time, they now face less inventory than they did one year ago.

The June market can be described as improving but still highly strategic. Buyers retain negotiating opportunities, while sellers benefit from stronger demand and reduced listing competition.

June 2026 Market Snapshot

The primary GTA market statistics for June 2026 were:

· Total home sales: 6,770

· Total sales dollar volume: $7,167,112,613

· Average selling price: $1,058,658

· Median selling price: $890,000

· New listings: 17,282

· Active listings: 27,329

· Sales-to-new-listings ratio: 36.5 per cent

· Months of inventory: 4.7

· Average sale-to-list price ratio: 98 per cent

· Average listing days on market: 29

· Average property days on market: 42

Compared with June 2025:

· Sales increased by 9.4 per cent

· New listings decreased by 12.9 per cent

· Active listings decreased by 13.5 per cent

· The average selling price decreased by 3.9 per cent

· Average listing days on market increased from 26 to 29 days

· Average property days on market remained unchanged at 42 days

On a seasonally adjusted basis, sales increased from May to June, while new listings declined. The seasonally adjusted average selling price and MLS® HPI Composite also increased slightly from May.

These month-over-month movements do not establish a complete price recovery. They do, however, support the conclusion that the market continued to tighten through the spring.

First Half of 2026 Results

During the first six months of 2026, the GTA recorded:

· 31,149 home sales

· $32,320,101,726 in total sales dollar volume

· An average selling price of $1,037,597

· A median selling price of $880,000

· 88,065 new listings

· An average sale-to-list price ratio of 98 per cent

· Average listing days on market of 31 days

· Average property days on market of 47 days

Year-to-date sales were slightly higher than during the first half of 2025, while new listings were substantially lower. The year-to-date average price remained below the corresponding 2025 level.

The pattern across the first half of the year supports the view that 2026 has developed in two different stages.

The first quarter was slower, with limited transaction activity and considerable buyer caution. Conditions began to improve during the second quarter as more purchasers moved forward with buying decisions.

The market has not returned to the rapid pace experienced during previous high-growth periods. The improvement is more measured. Buyers are participating, but they continue to negotiate and compare properties carefully.

Demand Strengthened Across the GTA

The 9.4 per cent year-over-year increase in sales is the clearest evidence that buyer activity improved.

The City of Toronto recorded 2,443 sales in June 2026, compared with 2,303 in June 2025. The rest of the GTA recorded 4,327 sales, compared with 3,888 one year earlier.

The average selling price in the City of Toronto was $1,081,375. The average across the rest of the GTA was $1,045,832.

These figures illustrate that the recovery in activity was not limited to one section of the region. Both the 416 and 905 areas contributed to the increase in transactions.

The strength of demand varied by property type, price range, municipality, and neighbourhood. Some areas showed relatively fast sales and strong sale-to-list ratios. Others retained more inventory and longer selling periods.

A GTA-wide increase in sales should therefore not be interpreted as proof that every local market performed equally. Local property type, price, condition, and competition remain central to the outcome of an individual transaction.

Supply Declined as Buyer Activity Increased

The decline in both new and active listings is particularly important.

New listings fell by 12.9 per cent year over year. This means fewer properties were added to the market during June than during the same month in 2025.

Active listings fell by 13.5 per cent. This suggests that available inventory was being absorbed while the flow of new supply was also reduced.

For buyers, lower inventory means fewer alternatives to compare. Buyers still had considerable choice across the GTA, but that choice was smaller than one year earlier.

For sellers, lower inventory can improve visibility. A property may face fewer direct competitors, particularly when it is located in a desirable neighbourhood and falls within an active price range.

Reduced inventory does not guarantee a successful sale. The average property still required 29 listing days and 42 property days to sell. Buyers continued to reject homes that did not offer sufficient value.

What changed was the direction of the market. Supply and demand were moving closer together.

If sales continue to increase while inventory continues to decline, negotiating conditions could gradually become more favourable for sellers. If new listings increase substantially, buyers may regain a larger selection of alternatives.

Interpreting the Sales-to-New-Listings Ratio

The GTA sales-to-new-listings ratio was 36.5 per cent in June.

This ratio compares completed sales with the number of new properties entering the market. It provides one view of the relationship between demand and new supply.

A ratio of 36.5 per cent indicates that buyers were not absorbing new listings at a pace that would create widespread seller dominance. There remained enough new inventory for buyers to compare properties and negotiate.

The importance of the June result lies less in the ratio alone and more in the surrounding movement.

Sales increased. New listings decreased. Active listings decreased. Seasonally adjusted sales also rose month over month.

Taken together, these results show a market that was tightening, even though buyers still retained meaningful choice.

Months of Inventory and Market Pace

The GTA recorded 4.7 months of inventory in June.

Months of inventory estimates how long it would take to sell the current active inventory at the existing pace of sales if no new listings were added.

The 4.7-month figure reinforces the view that the market remained relatively balanced and selective. It was not characterized by severe scarcity across the entire region.

However, the GTA average can hide substantial differences.

Durham Region recorded 3.4 months of inventory, while the City of Toronto recorded 4.7 months. York Region and Peel Region each had approximately 5.1 months. Halton Region had 4.3 months.

Within individual municipalities, the differences were wider. Some locations had less than three months of inventory, while others had considerably more.

This variation means a seller’s strategy should not be based on the GTA figure alone. A detached home in Whitby, a condo apartment in Toronto Central, and a luxury property in King operate within different buyer pools and inventory conditions.

Price Direction Remains Cautious

The average GTA selling price was down 3.9 per cent year over year, while the MLS® HPI Composite benchmark declined by approximately 5.4 per cent.

The difference between these measures is important.

The average selling price is influenced by the mix of properties sold. If a larger proportion of expensive homes sells during one period, the average may rise even when underlying values are relatively unchanged. If more lower-priced properties sell, the average may fall.

The MLS® HPI is designed to track the value of a typical property with consistent characteristics. It can provide a more stable indication of price movement across time.

Both indicators were lower than one year earlier, confirming that GTA prices remained under annual pressure.

The rate of decline, however, had moderated compared with earlier periods. The seasonally adjusted average price increased slightly from May to June, and the seasonally adjusted HPI Composite also moved slightly higher.

This suggests that the market may be approaching a period of greater price stability. It does not confirm that sustained appreciation has begun.

Further evidence would be required across several months, including continued sales growth, reduced inventory, improving sale-to-list ratios, and a consistent upward movement in benchmark values.

MLS® Home Price Index Results

The June MLS® HPI data showed annual declines across the major property categories.

For all TRREB areas:

· The Composite benchmark declined by approximately 5.4 per cent

· The single-family detached benchmark declined by approximately 5.3 per cent

· The single-family attached benchmark declined by approximately 5.1 per cent

· The townhouse benchmark declined by approximately 7.4 per cent

· The apartment benchmark declined by approximately 8.2 per cent

The larger declines in townhouses and apartments show that affordability-focused categories were not protected from price pressure.

In fact, condo apartment sales increased significantly while apartment benchmark prices remained well below last year. Buyers were willing to purchase more units, but they continued to demand lower prices.

This is a key feature of the June market: transaction activity improved before annual price growth returned.

Detached Home Market

Detached homes remained the largest segment of the GTA market.

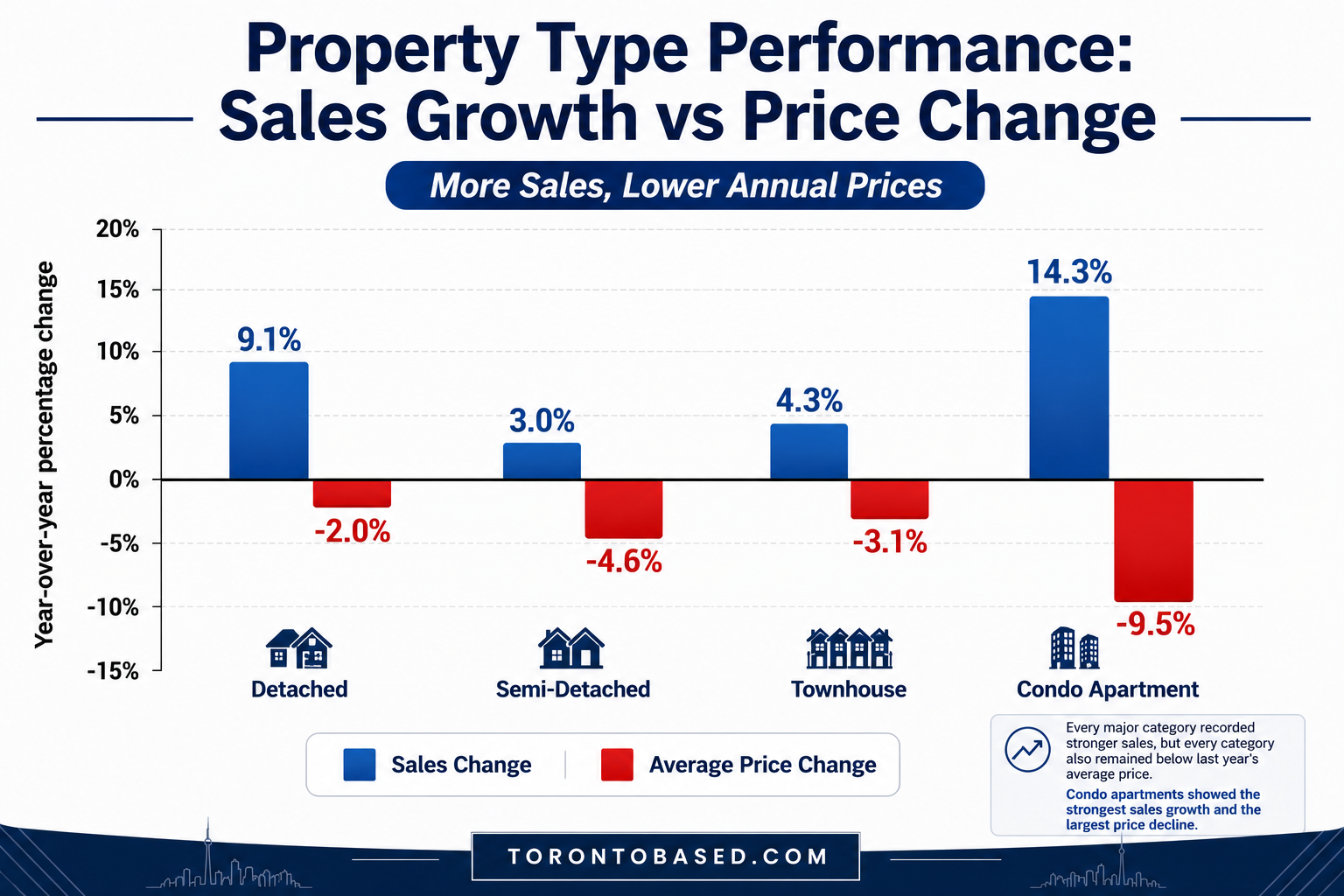

A total of 3,256 detached homes sold in June, accounting for 48.1 per cent of all transactions. Sales increased 9.1 per cent year over year.

The average detached price was $1,364,204, down 2.0 per cent from June 2025.

The geographic price difference was substantial:

· City of Toronto detached average: $1,648,440

· Rest of GTA detached average: $1,272,842

The detached market recorded:

· 8,470 new listings

· 12,635 active listings

· An average sale-to-list ratio of 97 per cent

· Average listing days on market of 25 days

· A median price of $1,160,000

Detached homes experienced the smallest annual average-price decline among the four major property types. This suggests that demand for traditional family housing remained comparatively resilient.

Sellers should not interpret this as unrestricted pricing power. Buyers paid an average of 97 per cent of the list price, showing that negotiation remained common.

Detached properties with desirable layouts, updated interiors, suitable parking, finished basements, strong school access, and competitive pricing were better positioned to attract attention.

Properties with significant renovation requirements or ambitious asking prices faced greater resistance.

Semi-Detached Home Market

A total of 617 semi-detached homes sold in June, an increase of 3.0 per cent year over year.

The average semi-detached price was $1,038,973, down 4.6 per cent from June 2025.

The City of Toronto average was $1,264,782, compared with $863,272 across the rest of the GTA.

The semi-detached market recorded:

· 1,218 new listings

· 1,480 active listings

· An average sale-to-list ratio of 102 per cent

· Average listing days on market of 19 days

· A median price of $910,888

The 102 per cent average sale-to-list ratio indicates that listing strategies within this segment often resulted in properties selling above their asking prices.

This does not mean every semi-detached home sold in competition. It may reflect the use of lower asking prices intended to attract multiple offers in certain neighbourhoods.

Semi-detached sellers should therefore evaluate both sale price and list strategy when reviewing comparable properties. A sale above asking does not automatically mean the property sold above market value.

Townhouse Market

The broader townhouse category reported 1,082 sales, an increase of 4.3 per cent year over year.

The average townhouse price was $844,579, down 3.1 per cent.

The City of Toronto townhouse average was $973,232, compared with $808,495 in the rest of the GTA.

Within the attached or row townhouse category, 619 properties sold at an average price of $912,380. Condo townhouses recorded 463 sales at an average price of $753,933.

The difference between freehold-style attached townhouses and condo townhouses is important for buyers.

A freehold townhouse may involve fewer monthly fees but can require the owner to manage exterior maintenance directly. A condo townhouse may have a lower purchase price but includes monthly condominium fees and shared governance.

Buyers should compare the full cost of ownership rather than focusing only on the purchase price.

For sellers, the competing alternatives matter. A townhouse may compete with small detached homes, semi-detached properties, larger condo apartments, and other townhouse formats.

Pricing and presentation must account for what the same buyer can purchase elsewhere.

Condo Apartment Market

Condo apartments recorded the strongest increase in transaction activity.

A total of 1,714 condo apartments sold, up 14.3 per cent year over year. The average price was $630,688, down 9.5 per cent.

The City of Toronto average was $665,760, while the rest of the GTA averaged $563,874.

The condo apartment market recorded:

· 4,550 new listings

· 8,630 active listings

· An average sale-to-list ratio of 97 per cent

· Average listing days on market of 38 days

· A median price of $540,000

Condo apartments represented 25.3 per cent of total June sales.

The 14.3 per cent increase in transactions indicates that more purchasers were willing to enter the condo market. The 9.5 per cent decline in average price shows that affordability remained central to that activity.

Condo buyers were likely to compare multiple units and buildings before making decisions. Important factors include:

· Maintenance fees

· Unit size

· Parking and locker availability

· Building condition

· Reserve fund strength

· Floor plan

· Exposure and floor level

· Transit access

· Amenities

· Management quality

· Upcoming repairs or assessments

Condo sellers face a market where similar units can be compared closely. Professional photography, accurate measurements, clear fee information, proper preparation, and realistic pricing are especially important.

Regional Market Differences

The GTA is not one uniform housing market.

June statistics varied considerably across the major regions.

City of Toronto

The City of Toronto recorded:

· 2,443 sales

· An average price of $1,081,375

· A median price of $835,000

· 6,096 new listings

· 10,047 active listings

· 4.7 months of inventory

· A 99 per cent sale-to-list ratio

· 29 LDOM

· 38 PDOM

York Region

York Region recorded:

· 1,289 sales

· An average price of $1,169,958

· A median price of $1,050,888

· 3,293 new listings

· 5,302 active listings

· 5.1 months of inventory

· A 98 per cent sale-to-list ratio

· 29 LDOM

· 45 PDOM

Peel Region

Peel Region recorded:

· 1,167 sales

· An average price of $966,024

· A median price of $875,000

· 3,267 new listings

· 5,189 active listings

· 5.1 months of inventory

· A 98 per cent sale-to-list ratio

· 29 LDOM

· 48 PDOM

Durham Region

Durham Region recorded:

· 849 sales

· An average price of $856,170

· A median price of $805,000

· 2,049 new listings

· 2,637 active listings

· 3.4 months of inventory

· A 99 per cent sale-to-list ratio

· 24 LDOM

· 36 PDOM

Halton Region

Halton Region recorded:

· 785 sales

· An average price of $1,222,898

· A median price of $1,060,000

· 1,846 new listings

· 2,827 active listings

· 4.3 months of inventory

· A 97 per cent sale-to-list ratio

· 28 LDOM

· 41 PDOM

These results illustrate why local analysis is required before making a pricing or purchasing decision.

Durham had a lower average price and less inventory than several other regions. Halton had a higher average price and a lower sale-to-list ratio. York had higher prices and more inventory. Toronto contained large differences between West, Central, and East districts.

No regional average should be treated as a substitute for neighbourhood-level comparable sales.

Buyer Behaviour in June 2026

Buyers became more active, but they did not become careless.

The increase in sales confirms that more purchasers were prepared to complete transactions. The decline in average prices, the 98 per cent sale-to-list ratio, and the 29-day average listing period confirm that buyers continued to negotiate.

The modern buyer has access to extensive information. Buyers can compare:

· Active listings

· Recent sales

· Price reductions

· Listing history

· Property days on market

· Neighbourhood alternatives

· Property taxes

· Maintenance fees

· Renovation requirements

· Financing costs

This access to information affects how quickly buyers respond.

A home that is well priced and well presented may attract attention shortly after launch. A property that appears overpriced may receive few showings even when the broader market is improving.

Buyers are not simply asking whether they like a home. They are asking whether it represents better value than other available options.

Buyer Strategy

Buyers should approach the second half of 2026 with preparation rather than urgency.

Establish a Reliable Budget

The June dataset reported:

· Bank of Canada overnight rate: 2.3 per cent

· Prime rate: 4.5 per cent

· One-year mortgage rate: 5.49 per cent

· Three-year mortgage rate: 6.05 per cent

· Five-year mortgage rate: 6.09 per cent

Financing remained a major affordability consideration.

Buyers should understand the difference between the amount a lender may approve and the monthly payment they can manage comfortably.

Property taxes, utilities, insurance, condominium fees, repairs, transportation costs, and future maintenance should be included in the budget.

Review Comparable Sales

Asking prices do not establish market value.

Buyers should examine recent sales of properties with similar size, condition, location, lot, parking, and features.

Active listings are useful for understanding competition, but sold listings provide better evidence of what buyers have recently paid.

Understand Listing History

The difference between LDOM and PDOM can reveal important information.

A listing may appear new because it has been cancelled and relisted. The property may have been exposed to buyers for a longer period than the current listing indicates.

Reviewing the complete history can help buyers understand seller expectations and possible negotiating flexibility.

Move Decisively on Strong Properties

A market with fewer listings can create competition for the best homes.

Buyers should not assume that every seller will accept a substantial discount. A property that is priced accurately may attract multiple interested purchasers even when the GTA average remains below last year.

Preparation allows a buyer to act without making an emotional decision.

Seller Behaviour in June 2026

Sellers entered a more constructive market, but they still needed to earn buyer attention.

Higher sales and lower inventory created a stronger environment than one year earlier. Prices, however, remained below June 2025 levels.

A seller who focuses only on improving transaction activity may set an asking price above what current comparable sales support.

That can result in:

· Reduced showing activity

· Extended days on market

· Price reductions

· Cancellation and relisting

· Weaker negotiating leverage

· Buyer concern about the property

Improving market conditions should support a stronger strategy, not unrealistic expectations.

Seller Strategy

Use Current Evidence

Pricing should be based on recent local sales, current competition, market time, condition, and buyer response.

The original purchase price, renovation expense, mortgage balance, or desired proceeds do not determine current market value.

Prepare Before Listing

The first days of a listing often generate the greatest attention.

Before launch, sellers should address cleaning, decluttering, repairs, staging, photography, descriptions, measurements, documents, showing arrangements, and marketing materials.

A listing should not be used to test the market before the property is ready.

Position the Property Clearly

Buyers should be able to understand quickly:

· What makes the property valuable

· How it compares with competing listings

· Which features are included

· Whether improvements were completed

· What costs are associated with ownership

· Why the asking price is reasonable

Clear positioning reduces uncertainty and strengthens buyer confidence.

Respond to Market Feedback

A listing strategy should be reviewed after launch.

Showing activity, online engagement, buyer comments, competing listings, new sales, and offers provide useful information.

If the market response is consistently weak, the seller should determine whether the problem relates to price, condition, access, presentation, or marketing.

Waiting without adjusting can reduce momentum.

Investor Considerations

June presented a combination of improving liquidity and lower annual prices.

More properties sold, which can make future resale easier if transaction activity continues to improve. Prices remained below last year, which may create acquisition opportunities.

The dataset does not include rental income, vacancy, operating costs, or property-specific financing. Those figures must be assessed separately.

Investors should evaluate:

· Purchase price

· Down payment

· Financing cost

· Property tax

· Insurance

· Maintenance

· Condominium fees

· Repairs

· Vacancy allowance

· Management expenses

· Legal use

· Expected rental income

· Holding period

· Exit strategy

A property should not depend entirely on future appreciation to justify the investment.

Improving market momentum is useful, but a strong investment must remain financially sustainable if prices stay relatively stable.

Market Risks

Several risks could alter the current direction.

New Listings Could Increase

Stronger sales may encourage more homeowners to list.

If new supply increases faster than buyer demand, inventory could rise and sellers could face greater competition.

Employment Conditions Could Affect Confidence

The dataset reported Toronto unemployment of 7.6 per cent and employment growth of 0.7 per cent.

Employment uncertainty can delay purchases, reduce borrowing capacity, and affect consumer confidence.

Inflation and Financing Remain Important

Inflation was reported at 3.2 per cent.

Even with a lower overnight rate, mortgage payments remain substantial. Financing qualification and monthly affordability may continue to limit buyer demand.

Price Expectations Could Move Ahead of the Market

If sellers raise prices before the data supports stronger values, sales momentum could slow.

A market can experience more transactions without immediate price appreciation. Pricing discipline remains essential.

What to Watch Next

The second half of 2026 should be evaluated through several connected indicators.

Sales

Continued year-over-year sales growth would support the view that buyer confidence is strengthening.

New Listings

A continued decline in new listings would place additional pressure on available supply. A substantial increase would give buyers more alternatives.

Active Inventory

Falling active inventory would indicate that demand continues to absorb supply.

Days on Market

A decline in LDOM and PDOM would suggest that properties are selling more efficiently. A growing gap between the two may indicate more cancellations and relistings.

Sale-to-List Ratio

A rising ratio would show that buyers are moving closer to seller expectations.

Average Price and HPI

These indicators should be reviewed together. Several months of consistent improvement would provide stronger evidence of price stabilization.

Property Type Performance

Condo apartments, townhouses, semi-detached homes, and detached properties may recover at different rates. Affordability will continue to influence where buyers concentrate their activity.

Practical Meaning for Buyers

June still provided buyers with opportunities.

Prices remained below last year. The market offered thousands of active listings. The average sale-to-list ratio remained below 100 per cent across the market as a whole.

Buyers should not interpret improving sales as a reason to rush. They should interpret declining inventory as a reason to become organized.

A financially prepared buyer can still negotiate while responding quickly when a suitable property is priced correctly.

Practical Meaning for Sellers

Sellers benefited from stronger demand and less active competition.

The opportunity was greatest for homes that entered the market with realistic pricing, professional preparation, and a clear marketing plan.

The June results do not support the assumption that all lost value has been recovered. The average price and HPI benchmark remained below last year.

Sellers should position their properties for the current market rather than pricing for a future recovery that has not yet occurred.

Practical Meaning for Investors

Investors may find opportunities where weaker annual prices overlap with improving sales activity.

The strongest acquisitions will be those supported by realistic cash flow, manageable financing, and a clear long-term strategy.

A tightening market may improve future resale conditions, but it should not replace property-level due diligence.

A Market Moving Toward Greater Stability

June 2026 showed that the GTA housing market was gaining momentum.

Sales increased by 9.4 per cent. New listings declined by 12.9 per cent. Active inventory fell by 13.5 per cent. Seasonally adjusted sales rose from May, while new listings declined.

Prices remained below last year, but the annual decline moderated and seasonally adjusted measures moved slightly higher month over month.

These conditions point to a market transitioning from weakness toward greater stability.

Buyers still have negotiating opportunities, but the supply of available homes is becoming smaller.

Sellers have a stronger opportunity to attract buyers, but pricing and presentation remain decisive.

Investors have access to lower annual prices and improving liquidity, but every acquisition must be supported by sound financial analysis.

Request a Personalized Market Analysis

GTA statistics provide important direction, but they cannot determine the correct value or strategy for one specific property.

Your neighbourhood, property type, size, condition, lot, renovations, parking, layout, comparable sales, and active competition all affect the result.

A personalized market analysis can provide:

· Recent comparable sales

· Current competing listings

· Local price trends

· Days-on-market patterns

· Property type performance

· Buyer demand

· Pricing position

· Preparation recommendations

· Marketing strategy

· Negotiation considerations

For a detailed review of your property, buying plans, or investment opportunity, request a personalized analysis based on the June 2026 market data and the most relevant local comparables.

The market is improving, but successful decisions still depend on understanding how the broader trend applies to your specific situation.

🏡 Ready to Start Your Real Estate Journey?

Whether you're planning to buy, sell, or invest, I’m here to guide you every step of the way — surprises and all.

📈 Looking to capitalize on today’s changing market?

Explore a wide range of specialized listings with access to powerful tools and search portals tailored to your needs:

· 🏢 Commercial & Industrial Properties

· 🏠 Residential Homes Across the GTA

· 🏨 Hotels & Motels Investment Opportunities

· 🏗️ Pre-Construction Condo Projects

· 🏙️ Condo Resale Listings in the GTA

Stay ahead of the curve. Get the latest real estate news and insights right here.

📩 Need help navigating your options?

Reach out for expert advice and market insights:

Sami Chowdhury

BROKER

📧 Email: samichy@torontobase.com

🌐 Web: www.torontobased.com | www.torontobase.ca

Let’s make your next move a smart one.

Get more market insights here:

· Renting vs. Owning: How $2,500/Month Could Cost You $190,000

· The GTA Housing Market Is Changing: What May 2026 Means for Buyers, Sellers, and Investors

· GTA Real Estate Market Update – April 2026

· Durham Region Real Estate Market Report – October 2025

· GTA Housing Market Update – August 2025

· Mississauga Condo & Condo Townhouse Market Report – Q3 2025

· Bill 60 vs. Ontario’s Residential Tenancies Act (RTA): What’s Changing?

Stay ahead of the curve. Get the latest real estate news and insights right here.